The Moment It Falls Apart

You've found the right person. Senior cloud architect, based in Manila, strong references, available in three weeks. You've done the hard part.

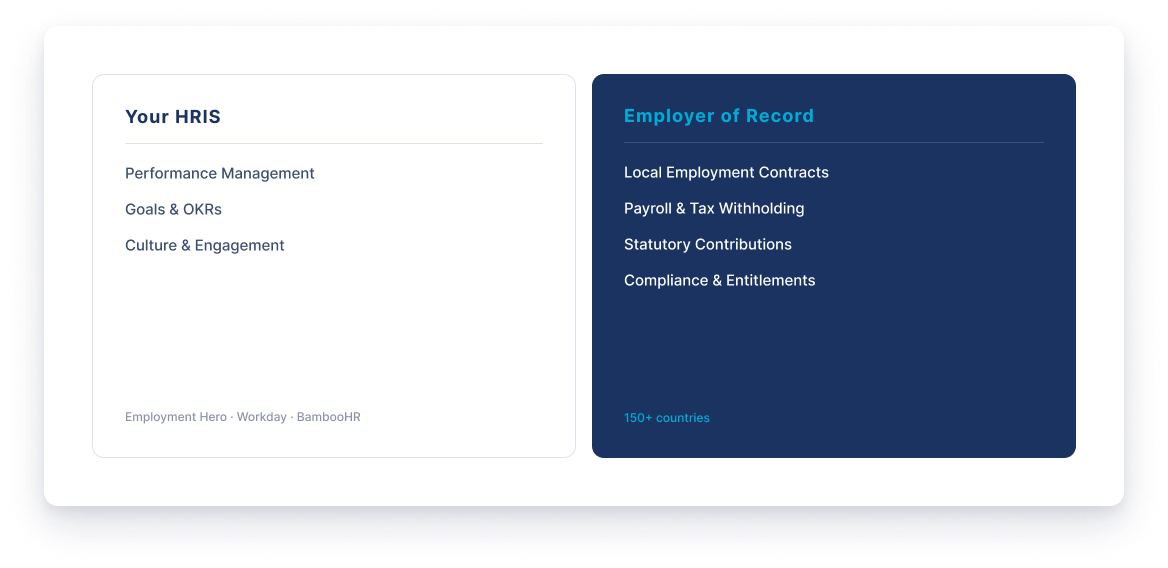

Then you open your HRIS - Employment Hero, Xero Payroll, MYOB, or even a more enterprise platform like Workday or BambooHR - and you need to set them up as an employee. There's no Philippine payroll entity. No SSS contribution calculator. No 13th month pay configuration. No field for DOLE-compliant probation terms.

This is the moment most Australian companies discover their HRIS was designed for one jurisdiction. Built for Australian employment law, and essentially silent on everything else. For a single overseas hire, the gaps are manageable - annoying, but manageable. For a company scaling a distributed team across three or four countries, those gaps compound into genuine operational and legal risk quickly.

Where It Actually Breaks

The problems cluster in a few predictable places, and they catch AU companies off guard consistently.

Leave entitlements

Australian employment law gives workers four weeks annual leave, ten sick days, and a handful of other entitlements most HR teams know by heart. The Philippines gives employees Service Incentive Leave (five days), solo parent leave, and paternity leave separate from maternity leave. India has earned leave, casual leave, and sick leave - typically accrued differently and governed state-by-state. Your HRIS leave policy is almost certainly not configured for any of this, which means leave balances are wrong from day one.

Superannuation equivalents.

Most countries have their own mandatory contribution schemes that function like super - they're just not called super. The Philippines has three: SSS, PhilHealth, and Pag-IBIG. Malaysia has EPF. India has Provident Fund and ESIC. Indonesia has BPJS. These contributions are mandatory, the rates are set by law, and remitting them on time is not optional. Your AU payroll system isn't calculating or remitting any of them.

Employment contracts.

A contract referencing Fair Work, the NES, and award conditions has no bearing on a worker in Bangalore or Warsaw. Local contracts need to reference local law, local minimum terms, and local termination conditions - which in many countries are significantly more protective of workers than AU equivalents. A contract that works perfectly for a Sydney employee is likely unenforceable for someone in Manila.

13th month pay.

In the Philippines, 13th month pay is not a bonus - it's a legal requirement, equivalent to one month's base salary, paid before December 24. You cannot contract out of it. It's been mandatory since 1975. Most Australian finance teams discover this the first Christmas they employ someone in Manila.

Tax withholding.

Your BAS process doesn't care about a Manila-based employee. But the Philippine Bureau of Internal Revenue does. So does the Indian Income Tax Department, and every other tax authority in every country where you have workers. Withholding the wrong amount, or failing to file locally, creates back-tax liability that sits with the employee - and increasingly, enforcement risk that extends to the employer.

What Companies Actually Do

Left to their own devices, most Australian companies handle these gaps in one of three ways. None of them are good.

The most common is to classify the overseas worker as a contractor, sidestepping the payroll and entitlements problem entirely. This works until it doesn't. Worker misclassification in the Philippines, India, and most of Southeast Asia carries real penalties - back-pay liability for all withheld entitlements, statutory contribution arrears, and in some jurisdictions, personal liability for company directors. DOLE enforcement has increased materially over the past two years, with specific focus on foreign companies engaging Filipino workers as "freelancers" to avoid statutory obligations.

The second approach is to engage a local accountant or HR provider in the target country to handle compliance manually. Better than nothing, but this creates a parallel people process sitting completely outside your HRIS - maintained by someone who has no visibility into your broader team operations. When that relationship ends, the institutional knowledge of what you've been doing in that country walks out the door with it.

"The companies getting global hiring right aren't relying on their HRIS to solve a problem it wasn't designed for. They've built the right infrastructure underneath it."

The third is the shadow spreadsheet. Many AU people teams running distributed workforces maintain a Google Sheet or Notion page tracking overseas entitlements, leave balances, and compliance dates that should be in the HRIS but can't be. This works until the person maintaining it changes roles, or until an auditor asks to see your employment records and finds a spreadsheet.

The Compliance Risk Is Real

This isn't just an operational frustration. The legal exposure from getting it wrong is material, and it tends to surface at the worst possible time - during a fundraise, an acquisition process, or an enforcement visit.

There's also an Australian angle that often gets overlooked: the ATO has guidance on when an overseas worker's activities create a permanent establishment risk in Australia. If your offshore team is effectively running core business operations rather than support functions, your company may have created a taxable presence in that country without intending to. This is a conversation worth having with your tax advisor before you scale past a handful of overseas hires, not after.

What the Right Infrastructure Looks Like

The solution isn't to replace your HRIS - it's to add an employment layer underneath it that handles everything local.

An Employer of Record provider takes on the legal employer relationship in each country where you hire. They handle the employment contract under local law, run the local payroll, remit statutory contributions, manage local compliance, and absorb the employer liability that comes with employing someone in a foreign jurisdiction. Your HRIS stays as your system of record for performance management, goals, and culture. It just doesn't need to know what EPF is.

The practical result: your AU-based people team manages a single, consistent employee experience through the tools they already know. The compliance complexity is invisible because it's handled. And when a regulator asks for employment records, there's a compliant local employer - your EOR partner - who can produce them.

This model scales in a way that local accountants and contractor arrangements don't. Whether you're employing three people in Manila or thirty, the infrastructure is the same. The marginal cost of adding a new country is lower than standing up your own entity, and the compliance risk is transferred rather than accumulated on your balance sheet.

Before Your Next Offshore Hire

If you're planning your first overseas hire - or if you already have overseas workers and the gaps described above sound familiar - a few questions worth working through before you proceed:

Does your employment contract for overseas workers reference local law, or is it an Australian template with the country name swapped? Is your leave policy mapped to local statutory minimums, or are you applying AU leave rules to non-AU employees? Do you have a mechanism to calculate and remit statutory contributions in the target country? Have you spoken with your tax advisor about permanent establishment risk?

If the answer to most of those is "not yet," you're not unusual - but you are exposed. The companies that figure this out early move faster, hire more confidently, and don't end up rebuilding their employment infrastructure mid-scale when the stakes are higher.

If your offshore hiring is getting ahead of your compliance infrastructure, talk to the Outstaffer team. We handle employment in 150+ countries so you can focus on finding the right people - not navigating payroll rules in every jurisdiction they're in. Start with your first role free →

More from

Global Hiring

category

%201.svg)